Systemic Underpricing of NFTs and Blockchain-Enabled Research

Systemic Underpricing of NFTs and Blockchain-Enabled Research

Overeager economics students often have a heady belief that all problems can be solved with price changes. First year economics teaches basic concepts about supply and demand, that market-clearing prices maximize social welfare, and that everything can be priced a la Coase Theorem*. Students take these lessons and try to apply them to their daily lives. I don’t want to do my dishes – I should just pay my roommates to clean them. Frat parties struggle to maintain a balanced gender ratio – they should just pay girls to come. Concert tickets always sell out – they should just increase their prices.

*Pet peeve – I hate how social sciences overuse terms like “theorem” and “law”. In math, theorems are logical statements that are always true. In natural science, laws are always and exactly followed by the observable universe, except in the most extreme edge cases. But social science throws around “theorem” and “law” to add an air of credibility to loose patterns that are frequently violated.

In the real world, markets fail to clear all the time. Supreme-branded sneakers sell out within minutes. Urban daycares are over-subscribed with year-long waitlists. Trendy restaurants have hour-long lines. Clearly there is excess demand. Why don’t they just increase prices? Are they stupid?

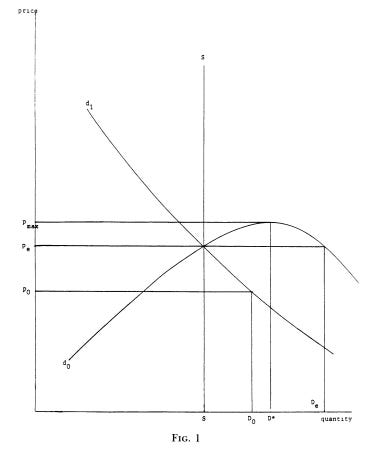

A perplexing puzzle for a pubescent economist. One answer comes from Gary Becker’s theory of “Social Influences on Price” wherein consumers gain additional utility if others also want the same thing. These “social goods” (not to be confused with public goods or social welfare) have a backward-bending demand curve, where they are either “in” or “out” of fashion. Reading this as an undergrad, I thought it was a curious thought experiment but chalked the results up to a modeling quirk. There was no empirical evidence to back it up.

d1 is the usual downward-sloping demand.

d0 adds social influences to create a backward-bending demand curve.

A relic from a bygone era when graphing software sucked

Enter NFT mania, when speculators run amok and FOMO is at an all-time high. Thousands of NFT collections launched with mediocre art and a dream. Most of them flopped, but some hit astronomic valuations. Curiously, NFT launches from established groups like Bored Apes seemed to be systematically under-priced and under-supplied, as the initial mint would sell out quickly and secondary market prices would shoot up. Why do these experts consistently under-price? Are they stupid?

They look pretty stupid.

According to “Digital Veblen Goods”, no, they are not stupid. The paper shows empirical evidence validating Becker’s social goods theory. NFT collections are bimodally “in” or “out” of fashion, and NFT issuers purposefully under-price to try to remain in fashion.

On one hand, these results are unremarkable to cryptoheads. Selling out on purpose to drum up FOMO and pop up in secondary markets is conventional wisdom. On the other hand, rigorous validation is quite significant for economics research. Theory makes predictions decades ahead of experimental evidence, be it black holes or Higgs bosons. Empirical validation is important to know that theory is on the right track. This paper is the first empirical and statistical evidence of the counterintuitive behavior of social effects.

Blockchain transparency was key in enabling this research. All transactions are recorded publicly, NFT token standards standardize the data, and tools like etherscan and dune analytics make it easy to dig up the data. In contrast, concert tickets and trendy restaurants are difficult to collect data on. Anecdotes abound, but collecting standardizing data across thousands of restaurants or ticket scalpers is nigh impossible. I am hopeful that blockchain data transparency will create more opportunities for research.

In fact, one of the “Digital Veblen Goods” authors has another paper utilizing blockchain data. “Evidence on Rational Token Retention” on ICOs (initial coin offerings) shows that token projects are more successful when the creators retain more tokens, likely due to aligned incentives or revealing greater confidence in the project. While this conventional wisdom has long existed for startup equity, blockchain data allows for more data transparency as well as removing confounding factors like regulation.

We’re interviewing one of the authors, Samuel Rosen, on the Game Economist Cast this upcoming Monday! If you’ve got any questions you’d like to ask, shoot them my way.